Now that home prices have escalated and most investors have slowed their buying frenzy, the banks have decided to welcome those with lower FICO scores and/or smaller down payments back into the real estate game. New lending guidelines make it easier for some to qualify.

Mortgage financing giants Fannie Mae and Freddie Mac, together with their federal regulator, have drawn up rules to loosen lending standards to

*They also would reduce the minimum down payment to 3% from the 5% generally needed to qualify.

*Fannie and Freddie’s guidelines set a minimum credit score at 620, once widely regarded as the cutoff between prime and subprime borrowers.

Tight lending standards have held back home purchases by average buyers in recent years, slowing the nation’s economic recovery. Isn’t this what got us in trouble before, believing the average buyer could be a homeowner? We revised lending standards, and then when they couldn’t make payments, we foreclosed and kicked them out of their homes.

Investors paying all cash for foreclosed properties buoyed housing markets for several years, but a decline in distressed sales and rising home prices have reduced those once-common transactions. Hedge funds were allowed to buy these distressed properties at steep discounts. Over the last three years, the F.H.A. has sold roughly 73,000 mortgages to private investors in a series of auctions. According to a RealtyTrac analysis, the loans have been sold at an average price of 62 percent of the estimated market value of the homes.

The low- to middle-income and minority borrowers are also the same people who were hit hardest in the mortgage crisis, said Paul Leonard, California director of the Center for Responsible Lending. “Understandably, the pendulum of mortgage credit standards swung to a far extreme after the crisis. It’s now working its way back to a more moderate position.” Yes, time to burn the same people who were hit hardest last time.

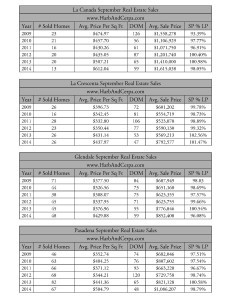

Real stories, real people:

In 2012, I sold a La Crescenta home to a teacher. Her down payment was 80%, and her credit score was in the high 700’s. Because her summer school income was off, getting her a loan was like pulling teeth. Fortunately, Floyd with BWA Mortgage was able to secure her financing. Being a mortgage broker, Floyd had a variety of sources.

In 2008, I sold a La Canada home to a self-employed buyer. Her down payment was 70%, and her credit score was in the mid-700s. Many self-employed people take a lot of write-offs, and qualifying them for a loan is often a challenge. Fortunately, she had an account with Merrill Lynch and could pledge assets.

We should loosen credit standards for those with good credit and large down payments. While new lending guidelines make it easier, if we wanted to help disadvantaged home buyers, we would have done so before prices escalated. Let’s hope real estate history isn’t doomed to repeat itself.

Related Stories:

Why Bernanke couldn’t get a refi?

Government Gives Big Edge to Large Investors in Florida Real Estate

Earlier this year, the Blackstone Group, the private equity and investment company that has bought 44,000 foreclosed homes since 2012 — more than any other institutional buyer — sharply scaled back its purchases. Today, the company is spending from $35 million to $40 million a week to buy homes, a considerable sum, but down from the $140 million a week it was spending last summer, said a person briefed on Blackstone’s strategy.